Sovereign Gold Bonds (SGB) are a popular and safe way of investing. Today, holding physical gold is always associated with some risk factors and also has a depreciation cost. On the other hand, if you want to hold a heavy amount in a safe, then locker charges are also required here.

The Sovereign Gold Bond Scheme 2023–24, Series I, was open for subscription. The issue, which opened on Monday, June 19, 2023, was closed on the next Friday. The date of issuance of the bond was on June 27. The SGBs will be issued in two tranches in FY24, as per the information available on the Reserve Bank of India (RBI) website. The Sovereign Gold Bond Scheme 2023–24, Series II, will be open for subscription on September 11 and close on September 15, 2023. The SGB will be issued on September 20, 2023.

By Reading this BLOG, You can explore all the details about SGB.

Before diving into the concept of Sovereign Gold Bonds, let’s first understand the term ‘bonds.’ Bonds are fixed-income instruments that government bodies or corporations issue if they need funds. And in return, these help investors add a component of stability to their financial portfolio.

The Central Government launched the Sovereign Gold Bond Scheme in 2015. The scheme opens for investment in tranches at different time windows, as per the announcement of the Reserve Bank of India (RBI).

A sovereign gold bond is a financial instrument issued by the RBI on behalf of the Government of India. The Sovereign Gold Bond scheme allows you to invest in gold without actually buying physical gold jewellery, coins, or bars. You earn a fixed interest rate of 2.5% per year and can even trade the bond on the stock exchange.

You can purchase the sovereign gold bond in cash and redeem it for the same when the bond reaches maturity. The issue price and redemption prices of SGBs are determined by calculating the simple average closing price of the last three working days of 999-purity gold as published by the Indian Bullion and Jewellers Association.

What is a Sovereign Gold Bond (SGB)? Who is the issuer?

SGBs are government securities denominated in grammes (g) of gold. They are substitutes for holding physical gold. Investors have to pay the issue price in cash, and the bonds will be redeemed in cash on maturity. The Bond is issued by the Reserve Bank on behalf of the Government of India.

Why should I buy SGB rather than physical gold? What are the benefits?

The quantity of gold for which the investor pays is protected since he receives the ongoing market price at the time of redemption or premature redemption. The SGB offers a superior alternative to holding gold in physical form. The risks and costs of storage are eliminated. Investors are assured of the market value of gold at the time of maturity and periodic interest. SGB is free from issues like making charges and purity in the case of gold in jewellery form. The bonds are held in the books of the RBI or in Demat form, eliminating the risk of loss of scrip, etc.

Are there any risks to investing in SGBs?

There may be a risk of capital loss if the market price of gold declines. However, the investor does not lose in terms of the units of gold that he has paid for.

As per 100 years of gold price data, investment in Gold always beats the Indian Inflation Rate. So, based on this historical data, it can be said that SGB is quite safe.

What are the minimum and maximum limits for investment in SGB?

What is the rate of interest, and how will the interest be paid?

The Bonds bear interest at a rate of 2.50 percent (a fixed rate) per annum on the amount of the initial investment. Interest will be credited semi-annually to the bank account of the investor, and the last interest will be payable on maturity along with the principal.

How is the value of SGB calculated?

The nominal value of the bond is based on the simple average of the closing price published by the India Bullion and Jewellers Association Ltd. (IBJA) for gold of 999 purity for the last three working days of the week preceding the subscription period. In this case, it is June 14, June 15, and June 16, 2023.

How do I buy SGB Online?

Want to invest in SGBs online? Are you worried that it will require a considerable load of paperwork and documents? Then you might be surprised to know that investing in SGBs is fairly simple and straightforward. You can invest in SGBs using online platforms and offline venues.

Online Investment in SGBs (Primary Issuance)

The procedure for investing in gold schemes through online platforms is short and straightforward. If you have an account at a listed commercial bank that offers services for online investment, then you can apply by following the instructions on the website.

You can also invest in SGBs through your broker in your trading account on the Broker’s Mobile App or Website.

As a measure to promote the digital purchase of SGBs, the issue price for online applications is Rs. 50 per gramme (g), less than the nominal value.

Offline Method to Invest in SGBs (Primary Issuance):

If you want to avoid online investing, you can Visit the nearest registered commercial bank, stockbroking agency, or post office. Ensure that they offer the Sovereign Gold Bond Scheme’s services.

Investment in SGBs through the Secondary Market

SGBs issued previously are listed on stock exchanges and are traded during market hours as normal stock trades. Investors who wish to invest in SGBs can also buy them through the secondary market. Generally, SGBs trade at a discount in the secondary market due to the low liquidity available.

You can invest in gold at a discount by buying SGBs in the secondary market.

Who is eligible to invest in the SGBs?

Persons resident in India as defined under the Foreign Exchange Management Act, 1999, are eligible to invest in SGB. Eligible investors include individuals, HUFs, trusts, universities, and charitable institutions. Individual investors with a subsequent change in residential status from resident to a non-resident may continue to hold SGB until early redemption or maturity.

What are the Know-Your-Customer (KYC) norms?

Every application must be accompanied by the ‘PAN Number’ issued by the Income Tax Department to the investor(s).

Investment Rules:

- You can invest in joint names, and the annual subscription limit only applies to the first holder.

- Minors can invest in gold bonds, and the guardian applies on the minor’s behalf with the required documents.

- Each family member can invest individually in their name under the specified annual limit.

- When you apply to the scheme, you will receive a unique investor ID that matches your identity documents. Subsequent investments will reflect the same unique ID for individuals and entities.

- If investing in Demat form, you must furnish your PAN number as a unique identifier.

Tenure

The tenor of the gold bond is eight years; early encashment or redemption of the bond is allowed after the fifth year from the date of issue on coupon payment dates. Further, the bond will be tradable on Stock exchanges if held in demat form.

Interest Payout

Physical gold appreciates over time as gold rates increase, but it doesn’t earn any return during the course of holding it. The principal remains locked until you sell the gold.

With gold bonds, you have the opportunity to earn a fixed interest rate of 2.5% per year on the amount of your initial investment. Interest will be credited semi-annually to the bank account of the investor, and the last interest will be payable on maturity along with the principal.

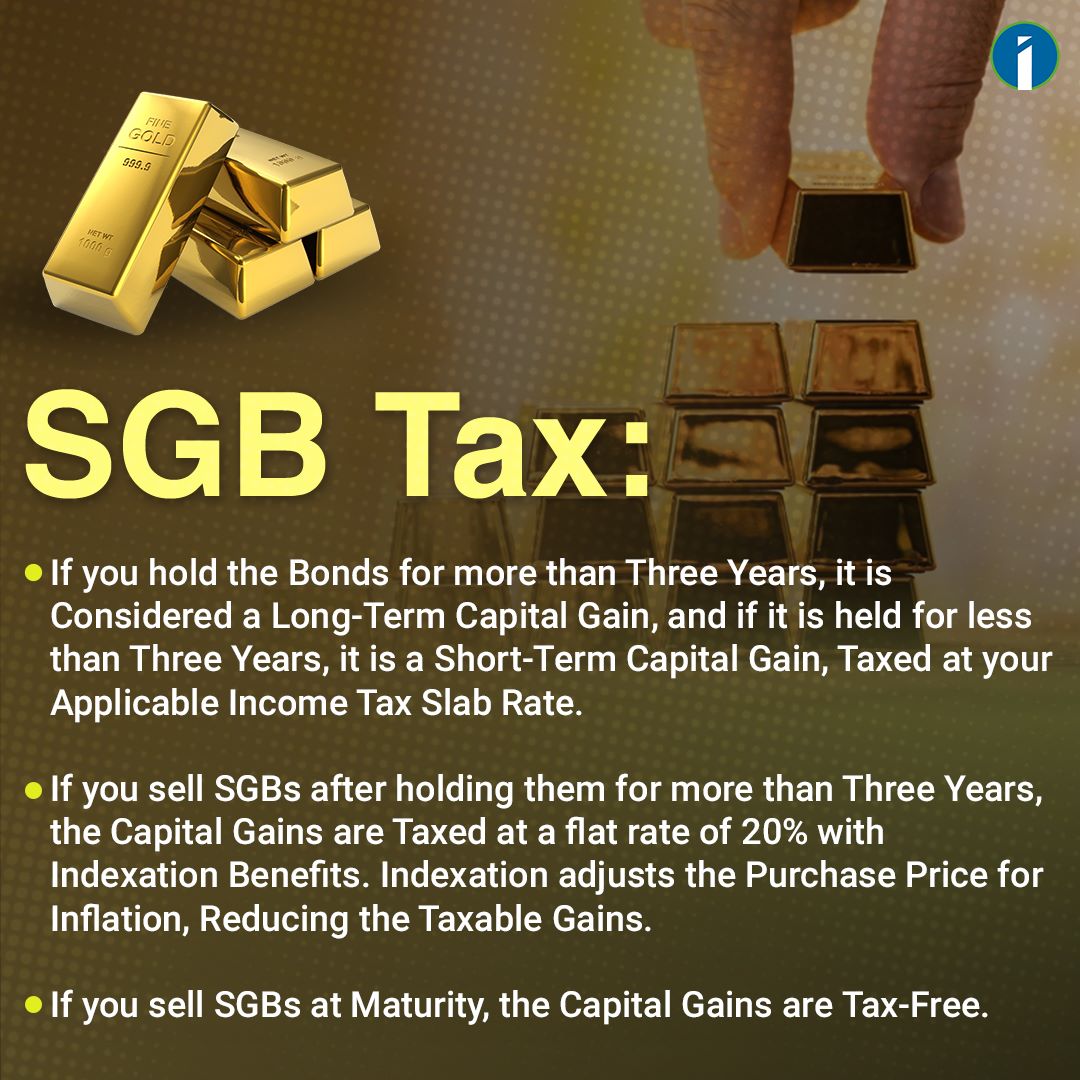

Tax Exemption

Acquisition: When you purchase SGBs, there is no tax on the purchase price. Interest Income: SGBs provide an annual interest rate. This interest is taxable as per your income tax slab rate. It is added to your income and taxed accordingly. If the interest income from SGBs exceeds Rs. 10,000 in a financial year, the issuer deducts TDS at the rate of 10% before disbursing the interest amount.

Gold is not just a precious metal; gold bonds make a great financial instrument for portfolio diversification. Governments and investors turn to gold when the tides are rough in the global economy. Sovereign gold bonds present an attractive opportunity to invest in gold as a hedge against turbulent times. By investing in gold bonds, you earn a fixed return on your pot of gold and capital appreciation! It’s a win-win for investors.

Hope, you will consider Sovereign Gold Bonds in future for investment and will take the Advantage from SGB investments.

If you Like our Informative Blog then please Like, Share and Comment.

এই তথ্য শুধুমাত্র শিক্ষামূলক উদ্দেশ্যে প্রদান করা হয়েছে। একে কোনোভাবেই Investment Advice বা Recommendation হিসেবে গণ্য করা উচিত নয়। আমরা একটি SEBI-registered Organization, এবং আমাদের মূল লক্ষ্য হলো বিনিয়োগ সম্পর্কিত Concepts-এর সাধারণ জ্ঞান ও বোঝাপড়া বৃদ্ধি করা।

প্রত্যেক পাঠক/দর্শককে অনুরোধ করা হচ্ছে, যেকোনো Investment Decision নেওয়ার আগে নিজস্ব Research এবং Analysis করুন। Investment সর্বদা হওয়া উচিত ব্যক্তিগত Conviction-এর ভিত্তিতে, অন্যের মতামত থেকে নয়। অতএব, প্রদত্ত তথ্যের ওপর ভিত্তি করে নেওয়া কোনো ধরনের Investment Decision-এর জন্য আমরা কোনোভাবেই Liability বা Responsibility গ্রহণ করি না।

very informative