The Income Tax Return (ITR) filing for the 2024-25 assessment year is in full swing, with about 4.76 lakh returns already submitted. Filing your ITR can feel overwhelming, especially if you’re unfamiliar with the process. Neglecting to file your ITR or submitting incorrect details can result in stressful notices from the Income Tax Department.

But don’t worry to make it easier for you, here are some key tips to ensure a smooth and hassle-free ITR filing experience.

Verify the correct ITR form

Different ITR forms are available based on your income source, income amount, and filing status. Selecting the appropriate form for your specific situation is crucial to avoid mistakes.

Types of ITR Forms for Income Tax Return Filing

- ITR-1: For resident individuals with income from salaries, one house property, other sources (interest, etc.), and total income up to ₹50 lakh.

- ITR-2: For individuals and HUFs not engaged in business or profession under any proprietorship.

- ITR-3: For individuals and HUFs with income from a proprietary business or profession.

- ITR-4: For individuals with presumptive income from business or profession.

Collect Form 16

- Form 16 is a TDS certificate from your employer for salaried individuals.

- It includes all salary details needed for filing income tax returns.

- It provides information on deductions claimed, salary earned, and exemptions availed.

Choose Wisely: Old Tax Regime vs. New Tax Regime

Perhaps the most important question for new taxpayers will be to figure out whether they want to opt for the new tax regime or the old regime. While the new tax regime offers lower tax rates, the old regime provides deductions and tax benefits that can help taxpayers save money.

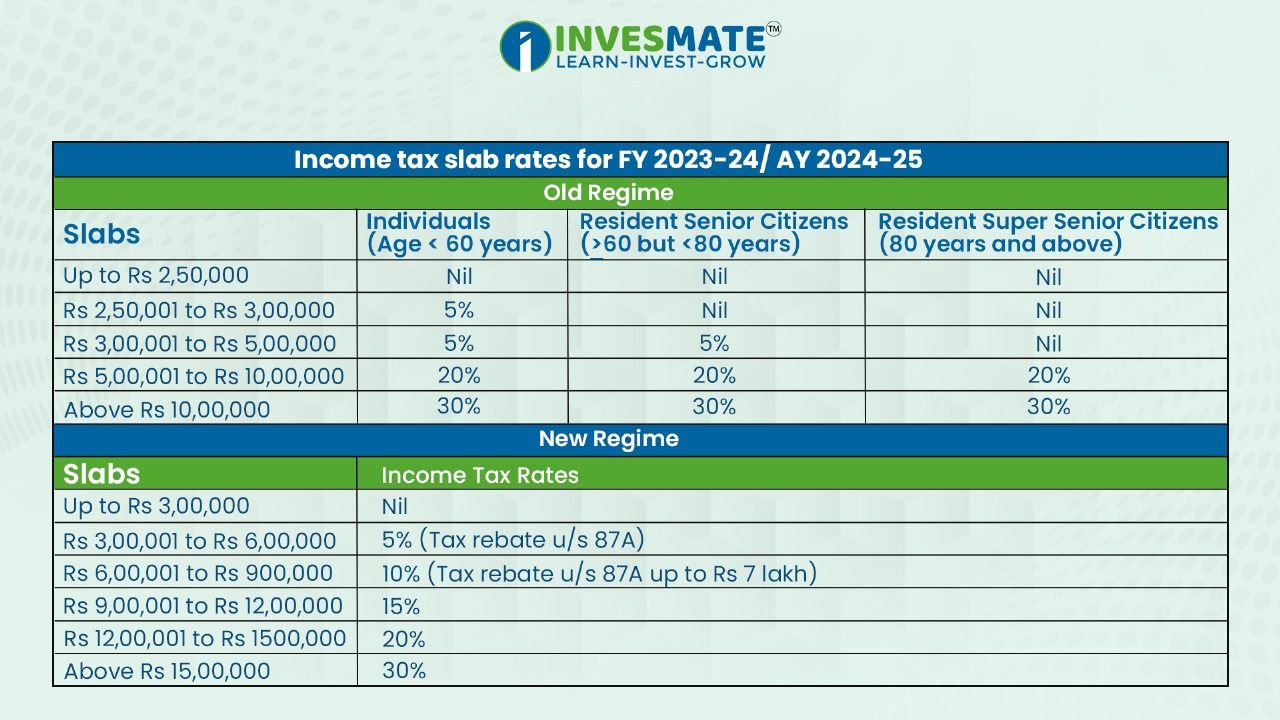

Income Tax Slabs

To assist you in choosing between the old regime and the new regime, we have detailed the Income Tax slabs below:

Capture all income sources:

- Accurately reporting all income sources is crucial for ITR filing.

- Failure to disclose incomes like salaries, investments, rental income, or interest from multiple bank accounts can trigger notices from the Income Tax Department.

Reconcile with Form 26AS/ AIS/ TIS

- AIS and TIS tools offer detailed data on financial transactions and tax-related information, crucial for ITR preparation.

- Form 26AS, originally a necessary document, now serves as a tax passbook displaying TDS and TCS details.

- Taxpayers should refer to both Form 26AS and AIS while filing their ITR to ensure all tax credits and deductions are accounted for.

Deadline

According to the latest regulations of the Income Tax department, failure to file their ITR by the deadline will automatically subject the taxpayer to the new tax regime.

The standard due date for filing your ITR is July 31st.

File your ITR on time to avoid late fees and interest. Filing early prevents last-minute rush and errors.

Conclusion

Filing your ITR in India can be overwhelming, but with preparation, it’s manageable. Remember, choose the right form, gather documents, understand income and deductions, meet deadlines, verify, e-file, and seek expert advice if needed. Stay tax-compliant and efficient!

FAQs

No, in the new tax regime, you cannot claim many deductions and exemptions available in the old regime, including those under Section 80C.

No tax is payable because there is a rebate available up to Rs. 5 lakhs in the old regime and up to Rs. 7 lakhs in the new regime.

ITR filing last date for Financial Year 2023-24 is July 31, 2024.

For incomes above ₹5 lakh, the penalty for filing ITR is ₹5,000 if filed before 31st December of the Assessment Year, and ₹10,000 if filed after 31st December but before 31st March of the Assessment Year. For incomes below ₹5 lakh, the penalty is ₹1,000.

An interest of 0.5% per month is paid from April 1 till the date on which the refund is granted. However, such interest is not payable when the tax refund is less than 10% of the total tax liability.

এই তথ্য শুধুমাত্র শিক্ষামূলক উদ্দেশ্যে প্রদান করা হয়েছে। একে কোনোভাবেই Investment Advice বা Recommendation হিসেবে গণ্য করা উচিত নয়। আমরা একটি SEBI-registered Organization, এবং আমাদের মূল লক্ষ্য হলো বিনিয়োগ সম্পর্কিত Concepts-এর সাধারণ জ্ঞান ও বোঝাপড়া বৃদ্ধি করা।

প্রত্যেক পাঠক/দর্শককে অনুরোধ করা হচ্ছে, যেকোনো Investment Decision নেওয়ার আগে নিজস্ব Research এবং Analysis করুন। Investment সর্বদা হওয়া উচিত ব্যক্তিগত Conviction-এর ভিত্তিতে, অন্যের মতামত থেকে নয়। অতএব, প্রদত্ত তথ্যের ওপর ভিত্তি করে নেওয়া কোনো ধরনের Investment Decision-এর জন্য আমরা কোনোভাবেই Liability বা Responsibility গ্রহণ করি না।

Leave a Reply