Kisan Vikas Patra is a government-backed flexible investment instrument offered in the form of certificates. The KVP scheme allows individuals to build wealth over time with minimal risk. It doubles your one-time investment in about 9.7 years (115 months). As per current rules, KVP certificates can be purchased from select public sector banks as well as from India Post Offices.

In this blog, we’ll cover the key features and potential benefits of this Kisan Vikas Patra (KVP) 2024 scheme.

What is Kisan Vikas Patra?

Launched in 1988 by India Post, the Kisan Vikas Patra (KVP) is a small savings scheme aimed to develop long-term saving habits. Initially targeted at farmers but it is now open to anyone meeting the eligibility requirements.

As per the latest update, the tenure for the scheme is now 115 months (9 years and 7 months).

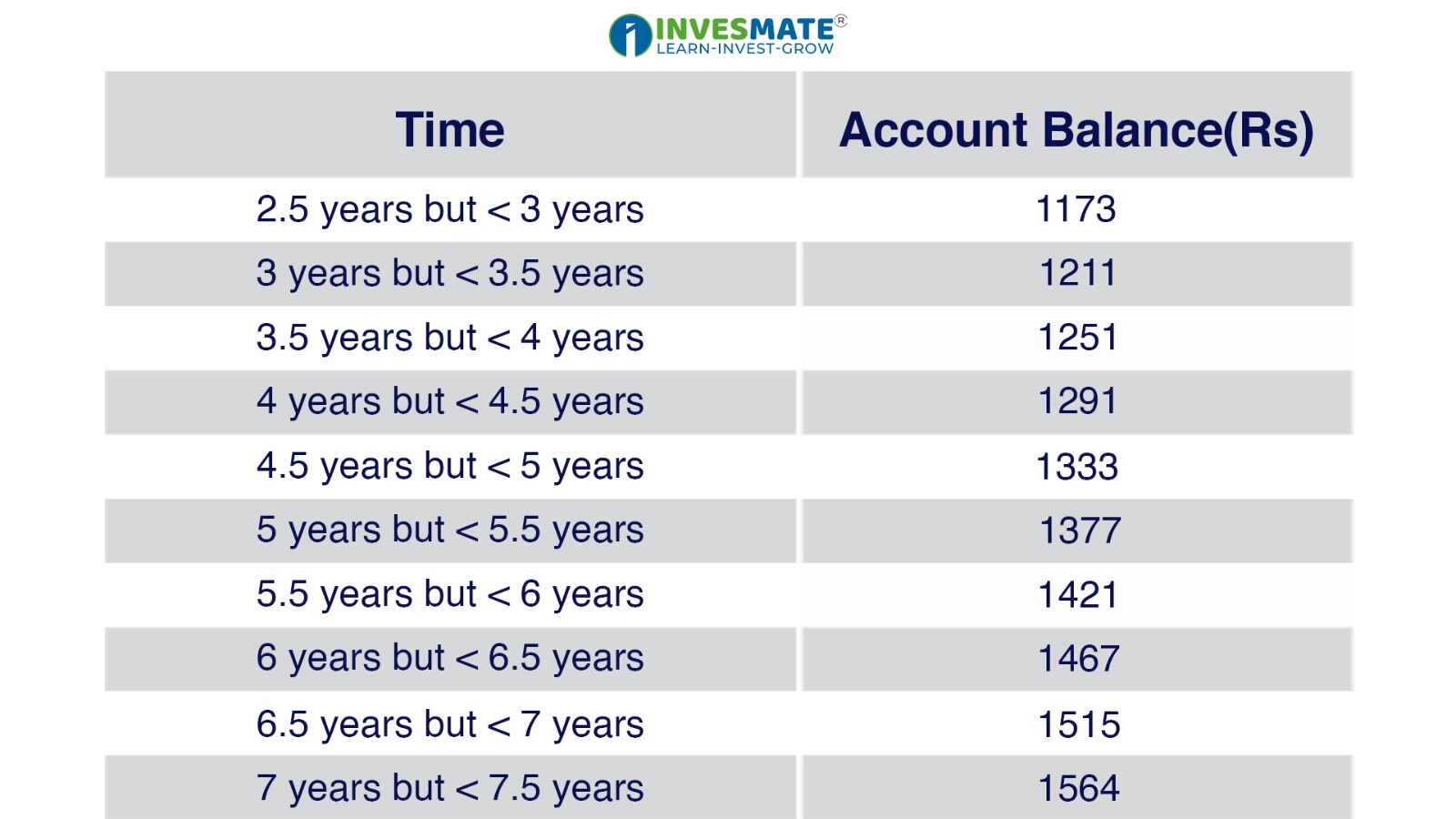

How KVP Accumulates Interest and Doubles Your Investment ?

KVP is a low-risk scheme. The table below illustrates the returns on an investment of Rs 1,000 over time.

Types of Kisan Vikas Patra Accounts

- Single Holder: Issued to an individual adult, either for themselves, on behalf of a minor, or directly to a minor.

- Joint A: Issued to two adults jointly, with payment made to both holders together or to the survivor.

- 3. Joint B: Issued to two adults jointly, with payment made to either holder or to the survivor.

Kisan Vikas Patra (KVP) Eligibility

- The applicant must be an Indian citizen and at least 18 years old.

- Adults can apply on behalf of minors or individuals with unsound mind.

- Hindu Undivided Families (HUF) and Non-Resident Indians (NRIs) are not eligible to invest in KVP.

Kisan Vikas Patra vs Fixed Deposits

A Fixed Deposit (FD) is a financial instrument offered by banks and NBFCs that provides higher interest rates than savings accounts. Here’s a brief comparison between KVP and FD:

Who Should Invest in the Kisan Vikas Patra Scheme?

KVP is ideal for risk-averse individuals with extra money they won’t need in the near future. The decision should align with your risk tolerance and financial goals.

How to Get Kisan Vikas Patra

- Offline: Visit a post office or selected bank, fill out Form A, submit KYC documents, and make the deposit.

- Online: Through the India Post website or internet banking, fill in the required forms and complete the KYC process.

Benefits of KVP Scheme

- Guaranteed returns, unaffected by market fluctuations.

- Interest is compounded annually.

- No TDS on withdrawals post-maturity, though no tax benefit under Section 80C.

- Loans can be taken against the certificate.

Premature Withdrawal and Transfer

- Premature withdrawal is allowed after 2 years and 6 months, only in specific cases like the holder’s death.

- KVP certificates can be transferred between individuals or post offices with a written request.

FAQs

If you’ve lost your KVPs, request a duplicate certificate from the issuing Post Office by submitting the identity slip given at the time of issue. If the slip is also lost, contact the Post Office for assistance.

Cooperative societies and cooperative banks are not allowed to invest in Kisan Vikas Patra (KVP).

The interest rate for this scheme is set at 7.5% for the first quarter of FY 2023-24.

The certificate holder can redeem a Kisan Vikas Patra at the bank or post office where it was originally issued.

এই তথ্য শুধুমাত্র শিক্ষামূলক উদ্দেশ্যে প্রদান করা হয়েছে। একে কোনোভাবেই Investment Advice বা Recommendation হিসেবে গণ্য করা উচিত নয়। আমরা একটি SEBI-registered Organization, এবং আমাদের মূল লক্ষ্য হলো বিনিয়োগ সম্পর্কিত Concepts-এর সাধারণ জ্ঞান ও বোঝাপড়া বৃদ্ধি করা।

প্রত্যেক পাঠক/দর্শককে অনুরোধ করা হচ্ছে, যেকোনো Investment Decision নেওয়ার আগে নিজস্ব Research এবং Analysis করুন। Investment সর্বদা হওয়া উচিত ব্যক্তিগত Conviction-এর ভিত্তিতে, অন্যের মতামত থেকে নয়। অতএব, প্রদত্ত তথ্যের ওপর ভিত্তি করে নেওয়া কোনো ধরনের Investment Decision-এর জন্য আমরা কোনোভাবেই Liability বা Responsibility গ্রহণ করি না।

Leave a Reply